TAX INFLATION ADJUSTMENTS1

The Internal Revenue Service announced the tax year 2026 annual inflation adjustments, including the tax rate schedules and other tax changes. The tax year 2026 adjustments described below generally apply to tax returns filed in 2027.

The tax items for tax year 2026 of greatest interest to most taxpayers include the following dollar amounts:

The personal exemption for tax year 2026 remains at 0. The elimination of the personal exemption was a provision in the Tax Cuts and Jobs Act of 2017 and was made permanent by OBBB. (The personal exemption described here does not include the senior deduction added by OBBB.)

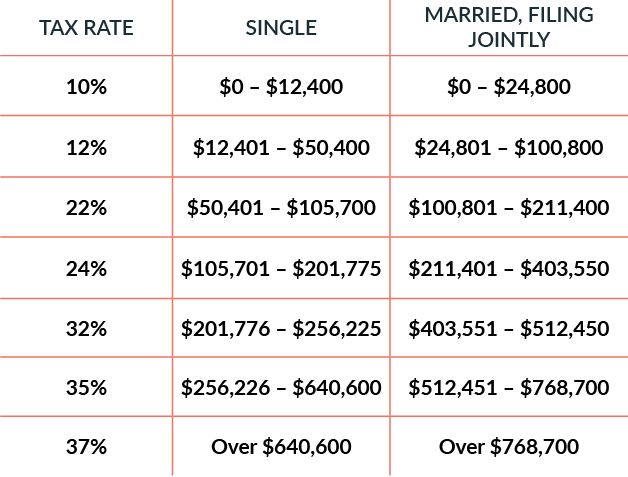

Marginal Rates: For tax year 2026, the top tax rate remains 37% for individual single taxpayers with incomes greater than $626,350 ($751,600 for married couples filing jointly).

The other rates are:

- The Alternative Minimum Tax exemption amount for exemption amount for tax year 2026 is $90,100 and begins to phase out at $500,000 ($140,200 for married couples filing jointly for whom the exemption begins to phase out at $1,000,000). For comparison, the 2025 exemption amount was $88,100 and began to phase out at $626,350 ($137,000 for married couples filing jointly for whom the exemption begins to phase out at $1,252,700).

- The tax year 2026 maximum Earned Income Tax Credit amount is $8,231 for qualifying taxpayers who have three or more qualifying children, an increase from $8,046 for tax year 2025. The revenue procedure contains a table providing maximum EITC amount for other categories, income thresholds, and phase-outs.

- For tax year 2026, the monthly limitation for the qualified transportation fringe benefit and the monthly limitation for qualified parking increases to $340, an increase of $15 from the limit for 2025.

- Health flexible spending cafeteria plans. For the taxable years beginning in 2026, the dollar limitation for employee salary reductions for contributions to health flexible spending arrangements increases to $3,400. For cafeteria plans that permit the carryover of unused amounts, the maximum carryover amount is $680, an increase of $20 from taxable years beginning in 2025.

- For tax year 2026, participants who have self-only coverage in a Medical Savings Account the plan must have an annual deductible that is not less than $2,900, an increase of $50 from tax year 2025, but not more than $4,400, an increase of $100 from tax year 2025. For self-only coverage, the maximum out-of-pocket expense amount is $5,850, up $150 from 2025.

For tax year 2026, for family coverage, the annual deductible is not less than $5,850, up from $5,700 for 2025; however, the deductible cannot be more than $8,750, up $200 from the limit for tax year 2025. For family coverage, the out-of-pocket expense limit is $10,700 for tax year 2026, an increase of $200 from tax year 2025.

- The annual exclusion for gifts increases remains at $19,000 for calendar year 2025.

- Adoption credits. The maximum credit allowed for adoptions for tax year 2026 is the amount of qualified adoption expenses up to $17,670, up from $17,280 for 2025.

RETIREMENT PLAN LIMITS2

Retirement plan contributions are tax-deductible. By putting money aside in a tax-advantaged retirement account, you are saving for your future and also reducing your taxable income. And remember, you have until April 15, 2026, to make your 2024 IRA plan contribution!

Catch-up Changes for 401(k), 403(b), governmental 457 plans and the federal government’s Thrift Savings Plans3

The catch-up contribution limit that generally applies for employees aged 50 and over who participate in most 401(k), 403(b), governmental 457 plans, and the federal government’s Thrift Savings Plan is increased to $8,000, up from $7,500 for 2025. Under a change made in SECURE 2.0, a higher catch-up contribution limit applies for employees aged 60, 61, 62 and 63 who participate in these plans. For 2026, this higher catch-up contribution limit remains $11,250 instead of the $8,000 noted above.

ROTH PLANS

For Roth accounts, you can only contribute to them if you make less than a certain amount of money. This salary amount was increased for 2026. Note that your contributions may be phased out at certain income levels so it is best to speak with your financial or tax advisor about your specific situation.

We know that proper tax planning is unique to every individual, and one strategy may not work for all. Our tax preparation services can help you optimize your taxes. Our certified tax preparers can not only help guide you through tax law changes but can also make sure you aren’t missing any deductions or credits.

The Tax Team provides the following services:

- e-file

- Same-day filing services

- 1040, 1040EZ, 1040x, Schedule A, C, & D

- Federal & State tax return preparation

CONTACT our tax specialists today to get started tackling your taxes.

SOURCES:

[1] https://www.irs.gov/newsroom/irs-releases-tax-inflation-adjustments-for-tax-year-2025

[2]https://www.irs.gov/retirement-plans/ira-year-end-reminders

[3]https://www.irs.gov/newsroom/401k-limit-increases-to-23500-for-2025-ira-limit-remains-7000