TAX INFLATION ADJUSTMENTS 1

Recently, the Internal Revenue Service announced the tax year 2022 annual inflation adjustments, including the tax rate schedules and other tax changes.

The tax year 2022 adjustments described below generally apply to tax returns filed in 2023.

The tax items for tax year 2023 of greatest interest to most taxpayers include the following dollar amounts:

- The standard deduction for married couples filing jointly for tax year 2022 rises to $25,900 up $800 from the prior year. For single taxpayers and married individuals filing separately, the standard deduction rises to $12,950 for 2022, up $400, and for heads of households, the standard deduction will be $19,400 for tax year 2022, up $600.

- Marginal Rates: For tax year 2022, the top tax rate remains 37% for individual single taxpayers with incomes greater than $539,900 ($647,850 for married couples filing jointly). The other rates are:

- 35%, for incomes over $215,950 ($431,900 for married couples filing jointly);

- 32% for incomes over $170,050 ($340,100 for married couples filing jointly);

- 24% for incomes over $89,075 ($178,150 for married couples filing jointly);

- 22% for incomes over $41,775 ($83,550 for married couples filing jointly);

- 12% for incomes over $10,275 ($20,550 for married couples filing jointly);

- The lowest rate is 10% for incomes of single individuals with incomes of $10,275 or less ($20,550 for married couples filing jointly).

- The tax year 2022 maximum Earned Income Tax Credit amount is $6,935 for qualifying taxpayers who have three or more qualifying children, up from $6,728 for tax year 2021. The revenue procedure contains a table providing maximum EITC amount for other categories, income thresholds and phase-outs.

- For tax year 2022, the foreign earned income exclusion is $112,000 up from $108,700 for tax year 2021.

- Estates of decedents who die during 2022 have a basic exclusion amount of $12,060,000, up from a total of $11,700,000 for estates of decedents who died in 2021.

- The maximum credit allowed for adoptions for tax year 2022 is the amount of qualified adoption expenses up to $14,890, up from $14,440 for 2021.

Read the full list of tax adjustments for 2022 at the IRS website.

TAX BREAKS 2,3

The tax law changed and you may not be aware of all the tax breaks you are eligible to receive. Some standard deductions continue to climb in 2022 by $400 to $12,950 for single taxpayers and married individuals filing separately; $19,400 for heads of households, up $600; and $25,900 for married couples filing jointly and surviving spouses, up $800 from the prior year.

- School Teachers Expenses: In 2022, qualifying teachers can claim $300, up from $250 in 2021, for expenses paid or incurred for books, supplies (other than nonathletic supplies for courses of instruction in health or physical education), computer equipment (including related software and services) and other equipment, and supplementary materials used in the classroom.

- Student Loan Interest: The $2,500 deduction for interest paid on student loans begins to phase out when modified adjusted gross income hits $70,000 ($145,000 for joint returns) and is completely phased out when MAGI hits $85,000 ($175,000 for joint returns).

- Health Savings Account (HSA): For 2022 there are higher HSA contribution limits available. You can contribute $3,650 for individual coverage for 2022, up from $3,600 for 2021, or $7,300 for family coverage, up from $7,200 for 2021.

- Charitable Donations: The $300 charitable deduction ($600 for joint filers) that was available to non-itemizers in 2021 has not been extended for 2022.

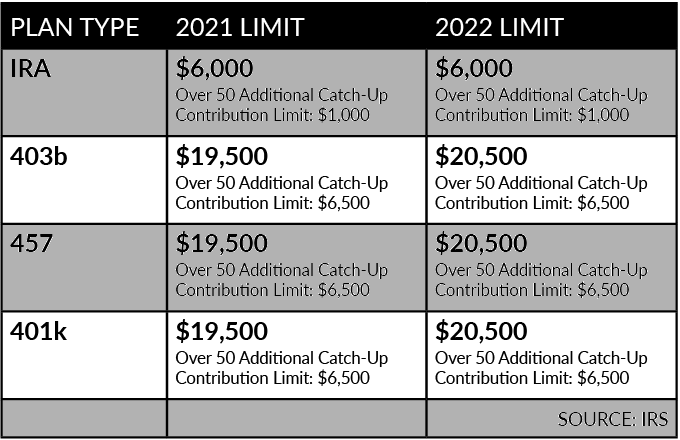

RETIREMENT PLAN LIMITS 4

Retirement plan contributions are tax deductible. By putting money aside in a tax advantaged retirement account, you are saving for your future and also reducing your taxable income. And remember, you have until April 15, 2022 to make your 2021 IRA plan contributions!

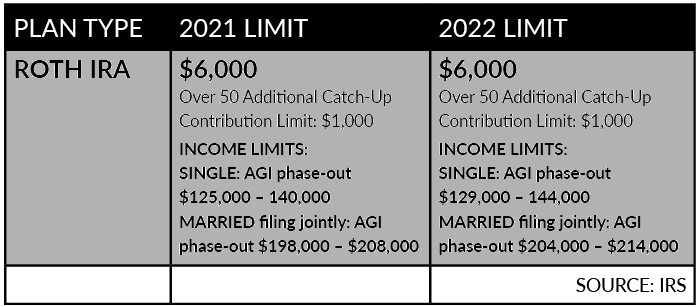

ROTH PLANS

For Roth accounts, you can only contribute to them if you make less than a certain amount of money. This salary amount was increased for 2022. Note that your contributions may be phased out at certain income levels so it is best to speak with your financial or tax advisor about your specific situation.

YEAR-END TAX OPTIMIZATION TIPS

With tax season well underway and returns fresh on our minds, we may be looking to how to minimize how much we will pay next year. Many money-saving tax strategies need to be implemented by December 31st to have an effect on tax filing in the spring.5

If you’re looking for ways to increase your savings and minimize the amount of federal income tax you’ll pay for 2021, talk to your tax professional about implementing some or all of these savings and tax strategies:

- DEFER INCOME: Consider opportunities to defer income to 2022, particularly if you think you may be in a lower tax bracket then.

- ACCELERATE DEDUCTIONS: If you itemize deductions, making payments for deductible expenses before the end of the year (instead of paying them in early 2023) could make a difference on your 2022 return.

- MAKE CHARITABLE CONTRIBUTIONS: You can generally deduct charitable contributions, but the deduction is limited to 60%, 30%, or 20% of your adjusted gross income (AGI), depending on the type of property you give and the type of organization to which you contribute.

- INCREASE WITH-HOLDINGS: If it looks as though you’re going to owe federal income tax for the year, consider increasing your withholding on Form W-4 for the remainder of the year to cover the shortfall.

- MAXIMIZE RETIREMENT CONTRIBUTIONS: Deductible contributions to a traditional IRA and pre-tax contributions to an employer-sponsored retirement plan such as a 401(k) can help reduce your taxable income. The window to make 2021 contributions to an employer plan generally closes at the end of the year, but you have until April 15, 2022, to make 2021 IRA contributions.

- TAKE YOUR RMD: If you are age 72 or older, you generally must take RMDs from traditional IRAs and employer-sponsored retirement plans. The penalty for failing to do so is substantial: 50% of any amount that you failed to distribute as required.

- YEAR-END INVESTMENT MOVES: If you have realized net capital gains from selling securities at a profit, you might avoid being taxed on some or all of those gains by selling losing positions. Any losses above the amount of your gains can be used to offset up to $3,000 of ordinary income or carried forward to reduce your taxes in future years.

We know that proper tax planning is unique to every individual, and one strategy may not work for all. Our tax preparation services can help you optimize your taxes. Our certified tax preparer can not only help guide you through tax law changes, but can also make sure you aren’t missing any deductions or credits.

The Tax Team provides the following services:

- e-file

- Same day filing services

- 1040, 1040EZ, 1040x, Schedule A, C, & D

- Federal & State tax return preparation

Even if you didn’t make all these money moves by December 31st for your 2021 taxes, you can start preparing to optimize your savings and taxes in 2022.

CONTACT our tax specialist today to get started tackling your taxes.

SOURCES:

- https://www.irs.gov/newsroom/irs-provides-tax-inflation-adjustments-for-tax-year-2022

- https://www.forbes.com/sites/ashleaebeling/2021/11/10/irs-announces-2022-tax-rates-standard-deduction-amounts-and-more

- https://www.ltcnews.com/articles/news/irs-reveals-2022-long-term-care-tax-deduction-amounts-and-hsa-contribution-limits

- https://www.irs.gov/newsroom/irs-announces-401k-limit-increases-to-20500

- https://pensionmark.com/year-end-2021-tax-tips/