The IRS has released the inflation adjustments for the 2026 tax year, reflecting modest increases in income tax brackets, standard deductions, and other key tax thresholds. These changes are designed to protect taxpayers from getting pushed into higher tax brackets despite no real increase in purchasing power.

Key Changes for 2026

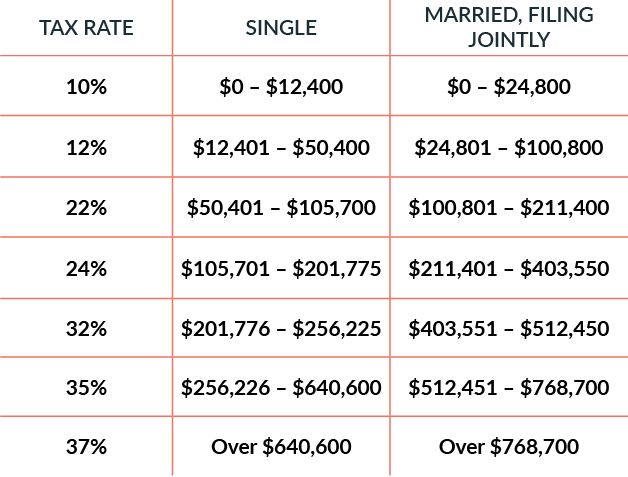

Here’s a breakdown of the new tax brackets:

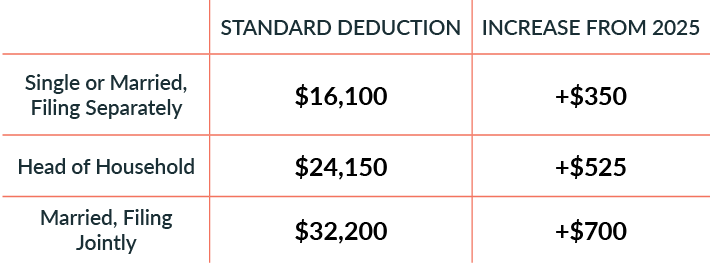

Standard Deduction. The standard deduction will rise to $16,100 for single filers, $32,200 for married couples filing jointly, and $24,150 for heads of households in 2026. This increase helps reduce taxable income, especially benefiting those who do not itemize deductions.

Additional Deductions for Seniors. Taxpayers aged 65 and older will see an increase in the additional standard deduction. This provides extra tax relief for older taxpayers.

Implications for Tax Planning

Income Management. The revised tax brackets allow those with incomes near the thresholds to avoid higher tax rates, which is crucial for year-end financial decisions regarding bonuses, capital gains, or other sources of income. Taxpayers can earn slightly more without facing an increase in their marginal tax rate.

Capital Gains Planning. While the inflation adjustments primarily impact ordinary income, they also affect capital gains planning. With the increased thresholds, taxpayers may have more room to realize capital gains at lower rates.

Estate and Gift Tax Planning. Although specific figures for estate and gift tax exemption amounts for 2026 have not been detailed, the trend is that these thresholds will also see inflation adjustments. Individuals engaged in estate planning should consider these updates in optimizing their strategies for maximizing exemptions and implementing effective gifting before year-end.

Retirement and Older Adults. The enhanced standard deduction and additional deductions for seniors underline the importance of tax planning for retirees, who may benefit from lower taxable incomes. These provisions can lighten the tax burden, particularly for years with varying income levels or required minimum distributions from retirement accounts.

Bottom line: The IRS’s adjustments for the 2026 tax year should help to mitigate the effects of inflation on tax liabilities. Staying informed and consulting tax professionals can help optimize financial decisions before the end of 2025 and ensure readiness for 2026 tax filings.